.png)

When a storm hits and the power goes out, business owners don’t just lose electricity. They lose revenue, time, and momentum.

And in a situation like this, it’s not uncommon to hear, “Your insurance policy doesn’t cover that.”

Unfortunately, that kind of response only makes a difficult situation even more difficult.

For many business owners, short-term weather disruptions like power outages, floods, or heat waves fall into a frustrating gap. Traditional insurance is built to handle the big, rare catastrophes. Not the quick, high-impact events that can throw off operations and cash flow.

But what if there was a smarter way to prepare for those gaps?

That’s where parametric insurance comes in.

Maybe you’ve heard the term, but what does it actually mean? And more importantly, how can it help your business stay resilient when the unexpected hits?

The Basics: What is Parametric Insurance?

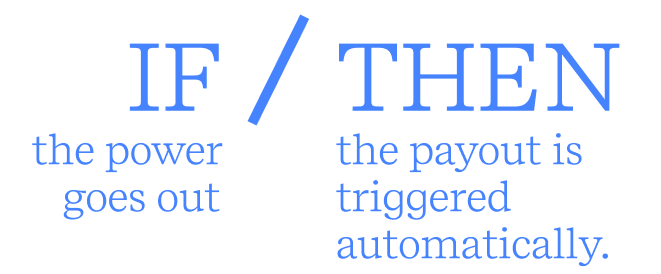

Think of it as “if/then” insurance. If the power goes out, then the claim is triggered, and you get paid.

That’s the idea behind parametric insurance. The name sounds technical, but the concept is simple and quick.

Unlike traditional insurance, there’s no filing a claim, waiting for an adjuster, or proving your losses. With “if/then” insurance, you agree on the trigger up front, and when it’s met, the payout is automatic.

And in most cases, that payout happens in just a few days.

It’s a model built for speed, clarity, and flexibility.

How Does It Work?

Adaptive’s policies are pretty typical of how a parametric insurance policy works. Here’s what happens:

- Agree on the event: You and Adaptive define a specific trigger. Like how many hours the power has to be out at your location before your business starts to feel the strain.

- Set the payout amount: Choose how much coverage makes sense if the event occurs. It may not make you whole, but it should be enough to keep a short-term disruption from turning into a long-term financial setback.

- Monitor real-time data: Adaptive uses sensors, weather feeds, and utility reports to track event data.

- Confirm the event: If the trigger is met, Adaptive verifies it automatically. No need to prove your loss or file paperwork.

- Get paid: The funds hit your account, often within just days. No adjusters, no paperwork, no headaches.

A Quick Example

Let’s say you run a restaurant in Texas, and a summer storm comes through and knocks out the power for 14 hours.

- You lose a day’s worth of reservations

- Your inventory spoils

- You send your staff home

Your traditional business insurance policy likely wouldn’t kick in unless the outage lasts 24 hours or more, and even then, there’s typically a long claims process involved.

But let’s say you have a GridProtect parametric policy that covers $10,000 when the power’s out for 12 hours or more.

So now? Your policy would pay $10,000 if there’s a power outage lasting 12 hours or longer. Real-time data would confirm the event, and within a couple of days, you would get paid. You can use the funds however you need to recover, keep the lights on, and keep moving forward.

Why It Matters Now

In the past, insurance was built around predictable patterns. Stable weather, consistent claims, and slow-moving disasters. But in the last decade or so, all that has changed.

We’re seeing…

- A 78% increase in power outages across the U.S.1

- $150 billion in losses annually from climate and weather-related events.2

- More volatility, more unpredictability, and more gaps in traditional policies.

What’s worse is that many of these events aren’t considered “catastrophic” enough to trigger standard business coverage. They are, however, disruptive enough to drain your cash flow and affect your business.

Parametric insurance helps fill that gap.

It’s designed for low-severity, high-frequency events. The ones that happen often and add up quickly.

What Makes Parametric Different from Traditional Insurance?

Traditional Insurance

- Requires proof of loss

- Adjusters and paperwork are involved

- Payout can take weeks or months

- Covers major losses only

- Can be vague or slow to respond

Parametric Insurance

- Pays based on predefined events

- No adjusters or loss documentation needed

- Payout typically in a few days

- Covers smaller disruptions that hurt most

- Transparent, fast, and trigger-based

It’s not better or worse. It’s just built for a different kind of risk. And in today’s business climate, both kinds of risk matter.

Who Is It For?

Adaptive's parametric insurance is especially valuable for properties with a physical location that rely on consistent daily revenue, time-sensitive operations, or perishable inventory.

It’s a great fit for…

- Restaurants, cafes, and food service businesses where inventory spoilage and lost service hours hit hard.

- Retail shops and salons with high-volume appointments or same-day bookings.

- Event venues and hospitality businesses where one canceled day equals thousands in lost revenue.

- Businesses in climate-sensitive regions (think Texas heatwaves, Gulf Coast storms, California wildfires).

If you’ve ever had to pay for emergency costs out of pocket or chase down a claim while juggling operations, you already understand the value of speed.

What It's Not

To be clear, parametric insurance isn’t meant to replace traditional insurance. It’s more of a complement or gap filler that addresses what most business owner policies overlook.

But parametric insurance can provide fast cash flow after a disruption, and freedom to use it however you need. That flexibility is key.

Real-World Disruptions, Real Business Impact

It’s not a once-in-a-decade disaster that poses the biggest threat to businesses.

It’s the smaller, more impactful disruptions that take a toll.

- A flash flood that shuts down your strip mall.

- A hard freeze that busts a pipe and pauses service.

- A heatwave that kills power on the busiest Saturday night of the month.

Any one of these might cost you $5k to $15k in lost business, and most traditional insurance won’t cover it.

What About Non-Admitted Insurance?

Most parametric products are offered through the E&S market (Excess & Surplus), meaning they’re non-admitted. That sometimes sounds risky to people unfamiliar with the term, but it’s not when structured right.

With Adaptive, for example:

- Policies are program-backed for long-term reliability.

- Payout triggers are clear and data-driven.

- Claims processes are streamlined and transparent.

You get the flexibility of E&S without sacrificing security.

The Bottom Line?

If you run a business, you already know it’s not the headline-grabbing disasters that cause the most stress.

It’s the frequent, smaller disruptions that eat away at your revenue and throw off your business.

And when those moments hit?

Tensions are high, customers are frustrated, and staff are waiting. The last thing you want to be doing is digging through policy documents or waiting weeks for a claim to come through.

Parametric insurance is built for that reality.

It’s fast, it’s fair, and it gives you back control when everything else feels out of it.

Find out more about how parametric coverage can fit into your current insurance plan. Contact us at hello@adaptiveinsurance.com.